Table of Contents

Social media advertising is a brand’s best bet for reaching new audiences (or even their existing followers!) in 2025.

That’s because adding a budget to your social strategy guarantees your social content will get in front of the people you want to reach. Plus, you can be very specific about which markets you want to target and how much you’re willing to spend compared to traditional advertising.

Keep reading to find out if social media advertising is a good fit for your business, how much you should set aside to get started, and which social networks to prioritize.

Bonus: We’ve even included expert tips from Hootsuite’s own Senior Manager of Paid Social, Cedric Bruce-Kotey.

Don’t feel like reading? Check out our top strategies and best practices for creating and optimizing GREAT social media ads:

Key Takeaways

- Social media advertising uses paid ads on platforms like Facebook, Instagram, and LinkedIn to target specific audiences more effectively than organic posts.

- Paid social ads help brands achieve specific goals, like increasing awareness, driving traffic, or boosting conversions.

- Most social platforms offer a variety of ad formats, including image, video, carousel, and Stories ads.

- Successful social ad campaigns require a clear objective, specific audience targeting, and regular performance monitoring.

- Important ad metrics to track include reach, engagement, click-through rate (CTR), and conversions. Use these to measure performance and refine future campaigns.

Social media advertising is a form of digital advertising in which advertisers pay to reach their target audiences on a social platform, like Facebook, Instagram, TikTok, LinkedIn or X.

The number of people who see your social media ads is referred to as your “paid reach.” This is in contrast to your “organic reach,” which refers to people who see your content as distributed by social media algorithms.

Social advertising is constantly evolving, too.

Standard Meta (then Facebook) ads are no longer the only way to reach users. Advertisers can now take advantage of the rise of new platforms such as TikTok, Snapchat, Reddit, and others that are constantly updating their advertising capabilities to stay competitive.

Why advertise on social media? Well, for starters, literally everyone else is doing it.

In fact, according to Sensor Tower, social channels make up the majority of ad spend in the US in 2024, with Facebook, Instagram, YouTube, and TikTok leading the way.

But that’s not the only reason you should invest in social ads. Here are three more benefits of social advertising:

- Specific audience targeting. The social platforms offer very detailed ad targeting. When you micro-target users with ad campaigns, you reach only the audience most interested in your products, which maximizes your ad spend.

- Real-time adjustments. Social ads provide instant feedback. You can easily gauge the effectiveness of an ongoing campaign and make changes based on performance, including reallocating budget to your best-converting ads with just a few clicks.

- Simple ROI tracking. It’s not always easy to calculate the return on investment (ROI) of your overall social strategy, but social ad metrics and reporting show you the real value of your work in dollars and cents.

To determine the most important places for you to advertise, you need to know which social media channels are most popular with your target market.

Which networks have the highest concentration of active users in your target demographics?

Here’s a quick summary of age demographics from the Pew Research Center, noting the percentage of U.S. adults who say they ever use a specific platform.

| Platform | Ages 18-29 | Ages 30-49 | Ages 50-64 | Ages 65+ |

|---|---|---|---|---|

| 67 | 75 | 69 | 58 | |

| 78 | 59 | 35 | 15 | |

| 32 | 40 | 31 | 12 | |

| Twitter (X) | 42 | 27 | 17 | 6 |

| 45 | 40 | 33 | 21 | |

| Snapchat | 65 | 30 | 13 | 4 |

| YouTube | 93 | 92 | 83 | 60 |

| 32 | 38 | 29 | 16 | |

| 44 | 31 | 11 | 3 | |

| TikTok | 62 | 39 | 24 | 10 |

| BeReal | 12 | 3 | 1 | <1 |

Source: Pew Research Center

Unsurprisingly, a large percentage of both Gen Z and millennials use YouTube and Instagram, while very few people over the age of 49 use Snapchat.

Of course, age is just one factor to consider when prioritizing your advertising on social media.

Not every channel is the right channel for you. It’s best to understand what value each channel provides and who your target audience is.

Where can you find the right audience interested in your product or service? What is your ideal demographic? Do you have enough budget to be on multiple channels without spreading yourself thin?

Once you have answers to a few of these questions, it’s easier to determine which platform to use.

For more demographics details, check out our full guide to social media demographics for marketers.

Here are the paid social media advertising campaign objectives and formats available on each of the major social platforms.

Facebook Ads

Facebook ads objectives

- Awareness: Introduce your brand to more people.

- Traffic: Send traffic to your website.

- Engagement: Bring in more likes, comments, and shares.

- Leads: Direct viewers to a lead-generation form.

- App promotion: Promote your app or game.

- Sales: Drive sales conversions.

Facebook ad formats

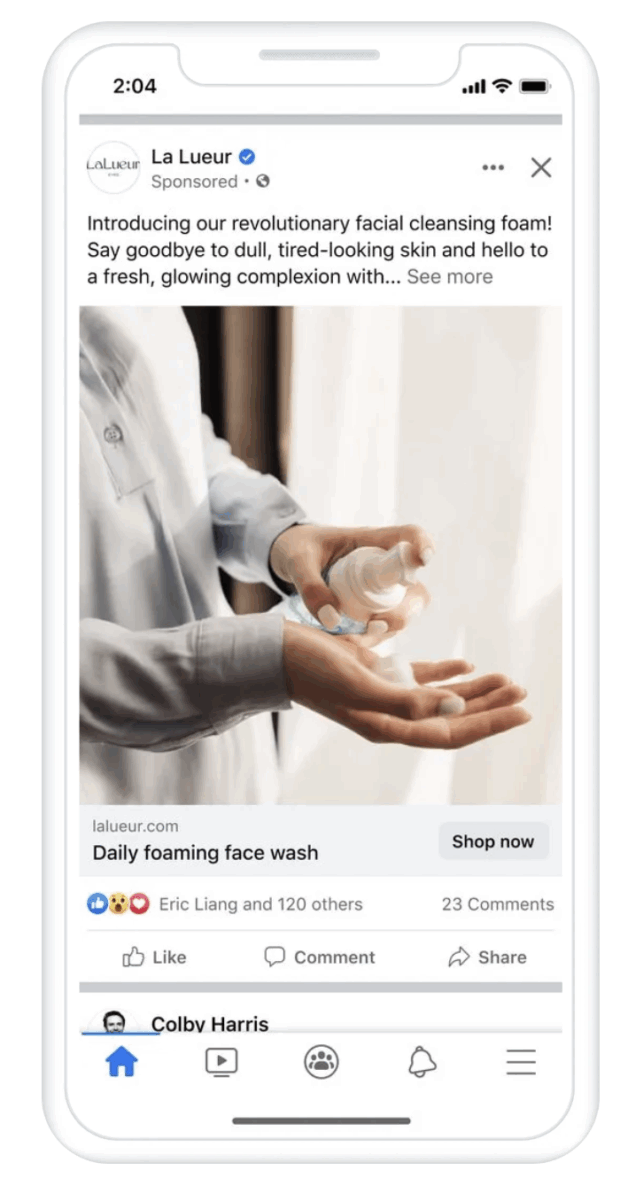

- Photo: A single image (not necessarily a photo) to promote your products, services, or brand.

- Video: Vertical or horizontal, for quick hits or deep dives.

- Stories: Mobile-only full-screen vertical video.

- Messenger: Viewers can tap to start a conversation with your brand.

- Carousel: Up to ten images or videos, each with its own headline, description, or link.

- Slideshow: Combine images and text to create a video ad that uses up to five times less data than regular video.

- Collection: Mobile shopping experiences that allow viewers to purchase directly through the app.

- Playables: Interactive previews of apps.

For more details, head over to our Facebook Advertising Guide.

Instagram Ads

Instagram ads objectives

- Awareness: Introduce your brand to more people.

- Traffic: Send traffic to your website.

- Engagement: Bring in more likes, comments, and shares.

- Leads: Direct viewers to a lead-generation form.

- App promotion: Promote your app or game.

- Sales: Drive sales conversions.

Instagram ads formats

These are mostly the same as the options for Facebook, as both types of ads can be created through Meta Ads Manager.

- Photo: A single image (not necessarily a photo) to promote your products, services, or brand.

- Video: Square or horizontal.

- Stories: Mobile-only full-screen vertical photos or videos that appear between Stories.

- Carousel: Up to 10 images or videos, each with its own headline, description, or link.

- Reels: Fullsceen vertical photos or videos that appear between Reels and in feed.

- Instagram Shop: Carousel or collection ads featuring square images and checkout through your website or within an Instagram Shop.

Read more in our guide to Instagram Advertising.

TikTok ads

TikTok ads objectives

- Reach: Introduce your brand to more people.

- Traffic: Send traffic to your website.

- Video views: Get more – you guessed it – video views.

- Community interaction: Increase traffic to your profile page

- Product sales: Drive sales conversions.

- Website conversions: Drive other conversions, like adding an item to cart or registering for your newsletter.

- Lead generation: Direct viewers to a lead-generation form.

- App promotion: Promote your app or game.

TikTok ads formats

- Image: A single full-screen image to promote your products, services, or brand.

- Video: A 5- to 60-second video.

- Carousel: Show between 2 to 35 images, depending on the selected objective. Clickable high-quality images or calls to action, also depending on the objective.

- Topview: A video ad shown as soon as someone opens TikTok. It starts with a 3-second video takeover that leads into an in-feed video. Only available through a sales representative for qualified customers.

- Spark ads: These are the TikTok version of boosted posts, with the added twist that you can boost posts from any creator (with their permission).

- Playable ads: Offer a preview of your app or game.

- Live shopping ads: Allows viewers to purchase products during a live stream.

- Video shopping ads: Create videos that allow users to purchase products from your catalog.

Learn more in our guide to TikTok ads

X (Twitter) ads

X (Twitter) advertising objectives

- Reach: Introduce your brand to more people.

- Video views: Get more video views.

- App installs: Promote your app or game.

- Website traffic: Send traffic to your website.

- Engagement: Bring in more likes, replies, reposts, and so on.

- App re-engagement: Get existing but infrequent users of your app to re-engage.

- Website conversions: Drive sales and other conversions, like adding an item to cart or registering for your newsletter.

X ads formats

- Promoted Ads: Formerly known as Promoted Tweets, these can be images, videos, carousels, or text-only.

- Vertical video ads: Full-screen, sound-on mobile ads. This is the fastest growing ad surface on the platform.

- Amplify: X Amplify Pre-roll ads appear before video content in 15+ categories.

- Takeover: X Trend Takeover allows brands to place a sponsored ad on the Explore tab, while X Timeline Takeover ads appear at the top of a user’s timeline when they open X.

- X Live: Ad budget to your X Live to maximize reach.

- Dynamic product ads: Retarget people who have engaged with a product on your website.

- Collection ads: A single hero image plus smaller thumbnails, with multi-destination linking.

Take a deeper dive into advertising on X.

Snapchat ads

Snapchat ads objectives

- Awareness: Introduce your brand to more people and drive traffic to your website.

- Snap promote: Promote a specific story to get more subscribers.

- Promote places: Advertise a physical location.

- App installs: Send viewers to the app store to download your app or game.

- Drive traffic to website: Send traffic to your website.

- Drive traffic to app: Promote your app or game.

- Engagement: Bring in more likes, comments, and so on.

- Video views: Get more video views.

- Lead gen: Direct viewers to a lead-generation form.

- Website conversions: Drive sales and other conversions, like adding an item to cart or registering for your newsletter.

- Catalog sales: Drive sales conversions from your catalog.

- App conversions: Drive conversions within your app.

- Calls and texts: Encourage viewers to call or text your business with a tap.

Snapchat ads formats

- Single image or video ads: A single image or video with a CTA.

- Collection ads: Four tappable product tiles to showcase products.

- Story ads: Between 1 and 20 single video or image ads, shown in sequence mimicking the experience of tapping through a Story.

- Lenses AR experiences: Interactive sponsored camera filters.

- Commercials: Ads up to 3 minutes long, with the first 6 seconds unskippable.

- Filter ads: Image overlays users can add to Snaps.

LinkedIn ads

LinkedIn ads objectives

- Brand awareness: Introduce your brand to more people

- Website visits: Send traffic to your website.

- Engagement: Bring in more likes, comments, shares, and so on.

- Video views: Get more video views.

- Lead generation: Direct viewers to a lead-generation form.

- Website conversions: Drive sales and other conversions, like adding an item to cart or registering for your newsletter.

- Job applicants: Promote job opportunities to qualified LinkedIn members based on skills and experience.

LinkedIn ads formats

- Single image ads: A single image to promote your products, services, or brand.

- Video ads: 3 seconds to 30 minutes in native video format.

- Carousel ads: Feature 2-10 clickable cards.

- Event ads: Drive attendance to an event with an ad that connects to your event landing page.

- Document ads: Share Word docs, PDFs, Powerpoints, and more, right in the feed – great for lead generation.

- Thought leader ads: Promote content from your brand’s thought leaders’ LinkedIn profiles.

- Sponsored Messaging: Send direct messages to your target audience’s LinkedIn inbox.

- Text Ads: A simple text-only format that appears in the right rail on desktop.

- Spotlight ads: Another right rail desktop ad, this time to highlight a specific product, service, or event.

- Follower ads: The final right rail desktop format, designed to bring in new followers.

Get all the step-by-step instructions in our LinkedIn advertising guide.

Pinterest ads

Pinterest ads objectives

- Brand awareness: Introduce your brand to more people

- Video view: Rather than just bringing in more views, this objective aims to maximize play times and completion rates.

- Consideration: Increase Pin clicks and outbound clicks.

- Conversions: Drive conversions like adding an item to cart or registering for your newsletter.

- Catalog sales: Drive sales conversions from your catalog.

Pinterest ads formats

- Image ads: A single image to promote your products, services, or brand.

- Video ads: You can choose either standard width or max width, which expands across the entire screen on mobile

- Carousel ads: Feature 2-5 images.

- Shopping ads: Single image ads designed to drive purchases.

- Collections ads: A single hero image plus three smaller thumbnails. Mobile-only.

- Idea ads: Multiple videos, images, lists, and texts in a single Pin.

- Showcase ads: Multiple cards, each with its own interactive features and links.

- Quiz ads: An interactive multiple-choice ad with options for multiple outbound links.

Learn more in our guide to Pinterest ads.

YouTube ads

YouTube ads objectives

- Awareness: Introduce your brand to more people

- Consideration: Make your brand top of mind when people start thinking about making a purchase

- Action: Drive sales and other conversions, like adding an item to cart or registering for your newsletter.

YouTube ads formats

- In-stream ads: Skippable or unskippable (up to 30 seconds) videos that run before, during, or after other videos.

- Bumper ads: Up to 6 seconds, non-skippable; these play before, after, or during another video.

- In-feed video ads: A thumbnail of your video plus text; these ads appear in search engine results, next to related videos, and on the mobile YouTube homepage.

- Masthead ads: Only available through a Google sales rep, these ads autoplay at the top of the YouTube desktop or mobile app.

Learn more about YouTube advertising.

1. Good Protein combines brand ads with creator content

The protein shake brand Good Protein ran a social media advertising campaign on TikTok in which they used Spark Ads to promote creator content alongside brand ads. Creators shared everything from recipes to reviews, while the brand answered questions through video responses.

Why this works: Social media users often trust creators more than brands themselves. Showcasing a variety of voices improved average watch time by 25%.

2. PureGym embraces “real Reels”

PureGym used lo-fi, handheld, Reels ads with text incorporated in the usual Reels style. The idea was to mimic the style of organic Reels content to increase watchtime and engagement.

Why this works: Brands can sometimes be tempted to make their ads look a little too slick. But it can be more effective to match the style of the typical organic content found on the surface you’re using. Going more casual gave PureGym a 5.6x increase in Thruplays over previous Reels ads. Bonus: The ads were cheaper and faster to create than their usual, more formal ads.

3. NARS Cosmetics boosts ROI with Instagram Shop ads

NARS Cosmetics tested shopping ads that allowed customers to check out via their Instagram Shop against ads that directed customers to the NARS website to complete their purchase. They found that adding the Instagram Shops checkout option increased ROI by 6% and decreased cost per purchase by 24%.

Why this works: This is a prime example of why testing is so important. The ad pointing customers to the NARS website was working just fine. Why mess with a good thing? Would customers be as willing to check out within the Instagram Shops interface? In fact, they were more willing to do so, something NARS would never have known without testing.

4. Cetaphil gets trendy on Pinterest

Cetaphil leaned into trending topics paired with the Pinterest Trend Badge to show Pinners that they were aligning their content (and new products) with statistically significant trends on the platform.

Why this works: Cetaphil put in the research before launching their campaign. They used keyword research to learn that people were searching for “simple skincare routine” and “skin types.” They used that information to inform their ad creative strategy, leading to a 4.5% increase in brand awareness.

Social media advertising cost in 2025

It’s nearly impossible to break down social media cost amounts in concrete terms. There are two main reasons for this:

- There are many variables in play, such as the value of the keywords you target, the time of year, and even the day of the week.

- None of the popular social media platforms tend to make this information public.

However, there are a few things we can say specifically. First, you need to understand how you are charged for paid social media advertising.

For most ad objectives (except off-platform conversion-oriented ones), you’ll pay either cost per thousand impressions (CPM) or cost per click (CPC).

For CPM: You pay every time someone sees your ad. Go ahead and cast a wide net to increase awareness.

For CPC: You don’t get charged for views, only for clicks. Include some qualifying text in your ad to make sure only valuable potential customers click through to reduce your social media advertising cost.

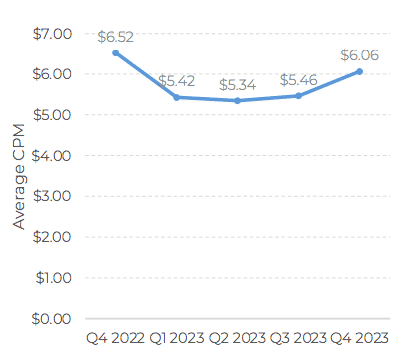

A couple of interesting things to note. First, CPM has been on a downward trend for the last year. For comparison, the CPM for paid social ads across Meta, Pinterest, TikTok, YouTube, and LinkedIn was $6.06 in Q4 2023, down from $6.52 in Q4 2022.

And here’s a look at how CPM varies across Meta ad surfaces. Reels have the lowest CPM, while the main feeds on Facebook and Instagram are the most expensive.

1. Let organic performance inform your ads

High-performing messages make the best candidates for social ads. In fact, the easiest way to advertise on social media is to boost a top-performing organic post.

Use what you’ve learned from your organic posts, user-generated content, or influencer partnerships as a starting point for your social media advertising strategy. Make sure to treat each platform as its own experiment, since results will vary depending on the audience. On that note…

2. Run A/B tests

Testing one ad against another to determine what works best and refine your strategy is known as A/B testing.

Optimizing ads is all about testing hypotheses. That means test, test, and test some more.

You need to determine which creative resonates best, explore new platforms your audience might be on, and take advantage of new features and placements that may help give you an edge.

It’s a best practice to test several ads with small audiences to determine what works best. Then, use the winning ad for your main social marketing campaign.

We teach you the details in our guide to social media A/B testing.

3. Know what business objective you’re trying to achieve

“Campaign ‘success’ can mean many things,” says Bruce-Kotey. “To determine success, you have to start with a clear goal or OKR.”

It’s no accident that we start each section of this guide by reviewing the business objectives each type of social media ad can help you achieve. It’s awfully hard to achieve your goals if you don’t know what your goals are in the first place.

Understanding your ultimate goal is critical. It ensures you choose the right social network to advertise on and find the right advertising solution within that platform. Your goal will even guide your creative strategy.

4. Know your target audience

Know exactly who you’re trying to reach to take maximum advantage of the targeting options and maximize your ROI.

Developing audience personas can help you understand exactly which audience segments to focus on.

Tip: If you have a brick-and-mortar business, try using “geofencing” to target mobile users so they only see ads when they are close enough to walk in your front door.

5. Measure results — and report on them

Having concrete data about how your ads contribute to business goals (purchases, leads, and so on) is a key part of proving (and improving) ROI.

Knowing which ads are most cost-effective will ensure you get the budget you need to continue your work.

The major social networks offer analytics to help you measure the results of ads.

You can also use tools like Google Analytics and Hootsuite Advanced Analytics to measure results across networks from a single dashboard. A social media report is a great way to track your results and look for great content to promote with social ads.

Manage social media advertising campaigns

When you manage your social ads alongside your organic content, you can clearly see the overall picture of your social content strategy. You can compare performance, juggle your budget, and really dig deep into the relative ROI of each campaign.

If you’re already using digital marketing tools like Mailchimp, Hubspot, or Salesforce, you can integrate those, too, so you have all your sales data in one place.

Here’s how to do it:

- From Hootsuite Composer, click Create, then choose the platform on which you want to run your campaign.

- Choose your objective, audience, budget, and timing.

- Add text and media to create your ad right in Composer. You can preview how it will look in different formats as you work.

- Submit your ad for review by the social platform.

- Once your campaign is running, use the analytics in Hootsuite Social Advertising to get detailed insights into the performance and ROI of your ad(s).

Manage boosted posts

The easiest way to create a social media advertisement is to boost a post. You can do this using native tools on some of the social platforms.

However, the more efficient way is to manage your boosted posts for Facebook, Instagram, and LinkedIn all from one place, alongside your organic content for all platforms in the Hootsuite dashboard.

Tip: Learn more about the difference between boosted posts and other kinds of advertising on social media.

You can schedule your boosted posts in advance as part of a campaign, and even set triggers so that your best organic posts are automatically boosted when they hit certain performance triggers.

If you have limited time (we see you, solo social media managers!), this is a hand-off way to expand your reach with social media advertising.

Here’s how to do it:

- In your Hootsuite dashboard, go to Advertise and select the type of post you want to boost: Facebook, Instagram, or LinkedIn.

- Choose your objective, audience, and placements, and click Boost (or Sponsor, for LinkedIn posts). That’s it!

Integrate your paid and organic social strategies to strengthen connections with existing customers and reach new ones. Use Hootsuite Social Advertising to easily keep track of all of your social media activity—including ad campaigns—and get a complete view of your social ROI. Try it for free.